What’s driving Australian home and investment loan interest rates at the moment?

Home loan and Investment loan interest rates in Australia are on the increase, yet the Reserve Bank of Australia (RBA) official cash rate has been on hold for a record 23 meetings in a row, at a record low of 1.50%.

While the RBA official cash rate is very important, domestic interest rates are influenced by a combination of factors. Two important factors are the banks exposure to domestic and offshore debt capital markets and, secondly, interest rates paid on deposits.

In essence, banks make profits on the net interest margin by charging borrowers a higher rate of interest than they pay on deposits and wholesale funding. If funding costs increase, the banks will typically look to pass through these higher costs to borrowers in the form of higher interest rates.

So why have some lenders increased mortgage rates recently when the RBA is on hold?

Almost all the banks have cited they have experienced an increase to their wholesale funding costs from the recent increase in the cash swap rate represented by the 3-month bank bill swap rate and their need to pass on these higher costs to borrowers, so their margins can be maintained.

The bank bill swap rate is the primary short-term reference lending base rate used in debt capital markets. The bank bill swap rate has been, on average, 0.20% wider than the RBA cash rate since 2003. However, it has recently spiked and currently sits 0.56% wider than usual levels, effectively adding 0.36% in additional wholesale funding costs.

Another driver has been the decline in deposit growth, forcing the banks to obtain higher levels of funding from domestic and offshore debt capital markets, along with the impact of quantitative tightening in the US and evidence that the RBA is less active in providing liquidity support through its open market operations.

Will rising rates in the US drive up mortgage rates in Australia?

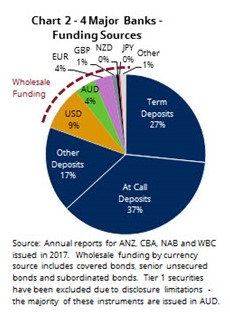

In the Australian economy, total bank loans exceed total deposits, resulting in the banks’ reliance on both domestic and offshore debt capital markets to fund the shortfall. When the balance sheets of the four major banks are consolidated together, 80.5% of total funding is sourced from deposits and the remaining 19.5% is sourced from debt capital markets (see chart below).

US dollar funding is the largest source of wholesale funding, making up 8.8% of total funding. When wholesale funding is issued, the banks will usually, at the same time, enter into derivative contracts to swap both the currency and interest rate exposure back to AUD and a margin over the Australian swap rate. This means the banks carry no ongoing exposure to both interest rates in the country of issuance, and corresponding exchange rates for offshore debt issuance.

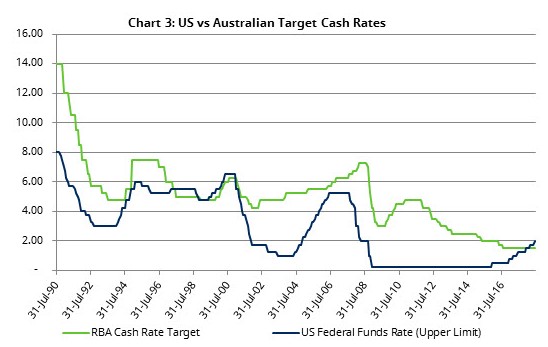

The US cash rate (Fed funds rate) moves independently of the RBA cash rate (see Chart below), reflecting differing economic growth and inflation expectations in each country. The Australian economy is now more closely linked to China than the US.

How are deposit rates impacting interest rates?

The recent changes in mortgage interest rates have been relatively small when compared to the fall in deposit rates, in particular rates paid on ‘at-call’ bank accounts, including online saver and cash management type accounts. Chart 4 highlights the 0.50% fall in online saving account interest rates in January 2018, a significant fall in relative terms but significant given at-call accounts are the largest category of bank funding, i.e. circa 37% of total funding. At-call savings accounts are now valued less by the banks given new liquidity regulations and that they are not as “sticky”.

Deposit holders have suffered a considerable decline in interest rates. In essence, the fall in deposit rates has limited further upward moves in mortgage interest rates, partially absorbing higher funding costs and the additional costs of tighter capital and liquidity requirements on banks. Simply put, borrowers have benefited to the detriment of deposit holders.

What is the most likely driver of mortgage rates in Australia going forward?

An increase in the official cash rate would have a significant and direct impact on mortgage rates. However, we anticipate that there will be no change to the cash rate, potentially for another 6 months or longer.

Higher offshore funding costs will adversely impact funding costs but only for incremental debt issuances and such increases take time to cycle through the entire wholesale funding profiles.

Higher deposit rates are probably the most likely to surprise the market, particularly if the current slowdown in deposit growth continues. Given deposit funding is such a large component of total funding, any increase in cost will have a proportionally larger increase in overall funding costs and place upward pressure on mortgage rates.

The bottom line is that, absent a rise in the official cash rate in Australia, any increase in Australian mortgage interest rates are likely to be modest.

Please do not hesitate to contact us if you have any questions.

Kind regards,

The Coastline Private Wealth Team.